Medical emergencies are one of the most expensive and stressful problems travelers face abroad. A sudden illness, injury, or accident can lead to hospital stays, emergency evacuations, and massive bills—especially outside your home country. Travel insurance plays a critical role in protecting you from these costs and ensuring access to care when you need it most.

This guide explains exactly how travel insurance covers medical emergencies, what is typically included, and where coverage limits apply.

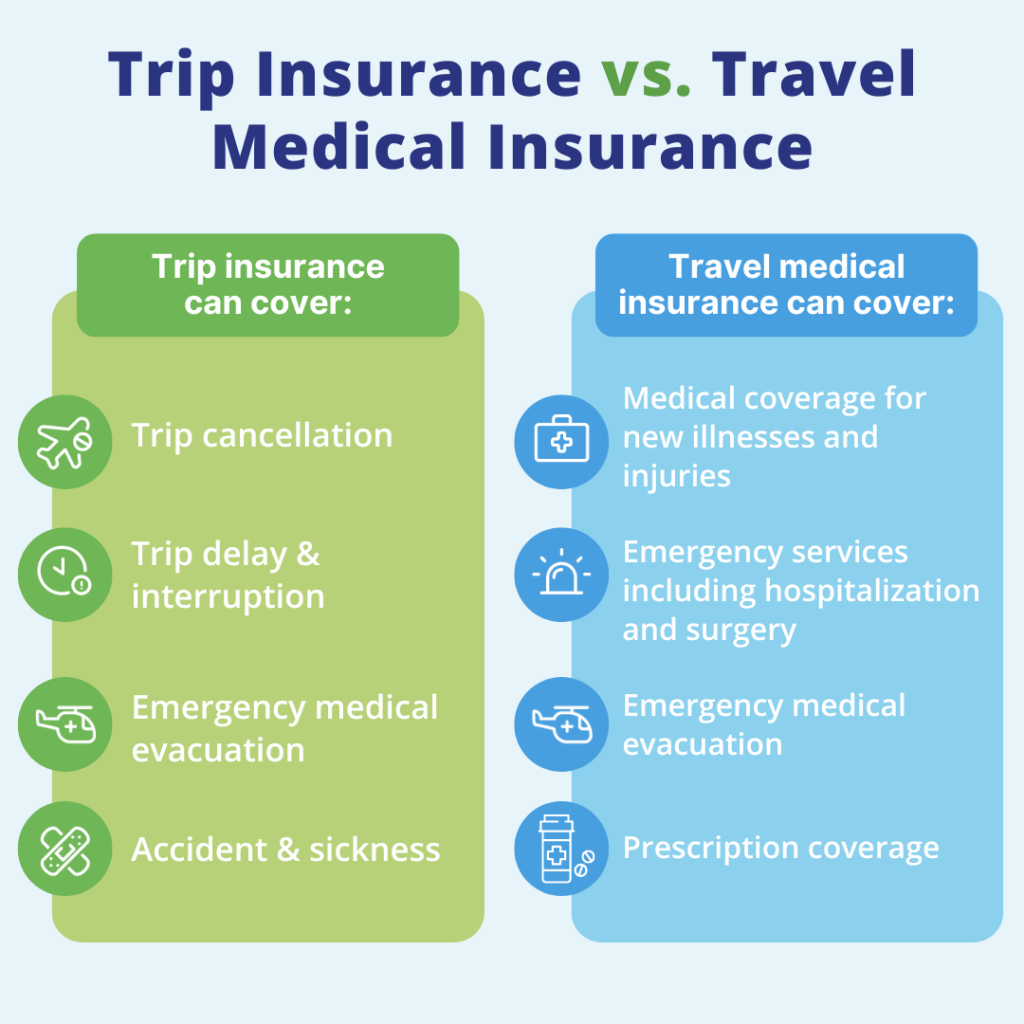

Why Medical Coverage Is Essential When Traveling

Most domestic health insurance plans provide limited or no coverage outside your home country. Even when coverage exists, reimbursement may be partial or require you to pay upfront.

Travel insurance fills this gap by providing immediate access to medical assistance and covering costs that could otherwise reach tens or even hundreds of thousands of dollars.

What Qualifies as a Medical Emergency

A medical emergency typically includes sudden and unexpected conditions that require immediate treatment, such as:

Serious illness or infection

Accidental injuries

Broken bones or severe sprains

Emergency surgeries

Life-threatening conditions

Routine or elective care is generally not considered an emergency.

Emergency Medical Treatment Coverage

Travel insurance usually covers:

Doctor visits and hospital stays

Emergency room treatment

Prescription medications related to the emergency

Diagnostic tests such as X-rays or scans

Coverage applies up to the policy’s medical limit, which varies by plan. Higher limits are strongly recommended for international travel.

Emergency Medical Evacuation

Medical evacuation is one of the most valuable benefits of travel insurance. If local medical facilities cannot provide adequate care, evacuation coverage pays for transportation to the nearest appropriate medical facility—or even back to your home country.

Evacuation costs can exceed $50,000 without insurance, making this coverage essential.

Repatriation of Remains

In the event of death while traveling, travel insurance typically covers the cost of returning remains to your home country. This benefit spares families from overwhelming logistical and financial burdens during an already difficult time.

Coverage for Pre-Existing Conditions

Most travel insurance policies exclude pre-existing conditions unless you qualify for a waiver. Waivers are often available if:

The policy is purchased shortly after the trip is booked

The traveler meets specific eligibility requirements

Failing to meet waiver conditions can result in denied claims.

What Medical Expenses Are NOT Covered

Travel insurance typically does not cover:

Routine checkups or preventive care

Elective or cosmetic procedures

Injuries from illegal or reckless activities

Medical issues related to substance abuse

Conditions excluded under the policy

Always review exclusions carefully before purchasing.

How Claims Are Handled During an Emergency

Many travel insurance providers offer 24/7 emergency assistance. In serious situations, they may:

Coordinate hospital care

Guarantee payment directly to providers

Arrange evacuation logistics

Assist with language barriers

For smaller claims, you may need to pay upfront and submit receipts for reimbursement.

Documentation Required for Medical Claims

To file a medical claim, insurers usually require:

Medical reports or doctor’s notes

Itemized bills

Proof of payment

Policy and travel details

Keeping copies of all documents speeds up claim processing.

How Much Medical Coverage Do You Need?

Recommended coverage depends on destination and risk level:

International travel: high medical limits

Remote destinations: strong evacuation coverage

Older travelers: higher medical limits

Adventure travel: confirm activity coverage

Choosing low limits may reduce premiums but significantly increases financial risk.

Common Mistakes Travelers Make

Assuming domestic health insurance applies abroad

Choosing minimal medical limits to save money

Ignoring evacuation coverage

Not disclosing medical history

Waiting too long to buy insurance

Avoiding these mistakes ensures your policy works when you need it.

Final Thoughts

Medical emergencies abroad can happen to anyone, regardless of age or health. Travel insurance provides more than reimbursement—it provides access, coordination, and protection when navigating unfamiliar healthcare systems.

When traveling internationally, medical coverage isn’t optional—it’s essential.