Choosing the right insurance deductible is one of the most important decisions when buying or renewing an insurance policy. The deductible directly affects how much you pay each month and how much you’ll owe out of pocket if you file a claim. Picking the wrong deductible can either strain your budget during a loss—or cause you to overpay in premiums year after year.

This guide explains how deductibles work and how to choose the best option for your financial situation.

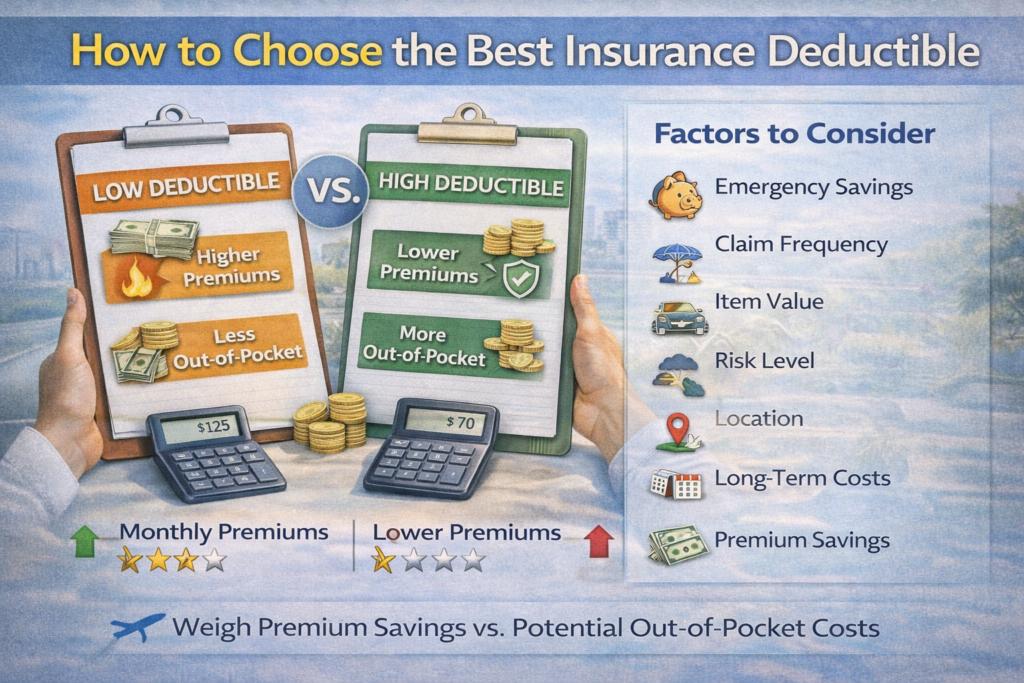

What Is an Insurance Deductible?

An insurance deductible is the amount you must pay out of pocket before your insurance coverage begins to pay. For example, if you have a $1,000 deductible and a covered loss of $6,000, you pay the first $1,000 and your insurer pays the remaining $5,000.

Deductibles apply to many types of insurance, including auto, homeowners, renters, health, and business insurance.

How Deductibles Affect Your Premium

There is a direct relationship between deductibles and premiums:

Higher deductible → Lower monthly or annual premium

Lower deductible → Higher premium

When you choose a higher deductible, you’re agreeing to take on more risk in exchange for lower ongoing costs. A lower deductible shifts more risk to the insurer, which increases your premium.

Common Deductible Options

Most insurers offer several deductible choices, such as:

$250

$500

$1,000

$2,500 or higher

Some policies, such as homeowners insurance in disaster-prone areas, may also use percentage-based deductibles.

Factors to Consider When Choosing a Deductible

Your Emergency Savings

The most important factor is how much you can comfortably afford to pay if a claim happens tomorrow. Your deductible should never exceed your available emergency savings.

If paying a $1,000 deductible would cause financial stress, a lower deductible may be the safer choice—even if premiums are higher.

How Often You File Claims

If you rarely file claims, a higher deductible often makes sense. You’ll save money over time through lower premiums.

If you expect frequent small claims, a lower deductible may be more practical.

Value of the Insured Item

For auto insurance, consider your car’s value. A very high deductible on an older vehicle may not be worth it if repair costs are close to the deductible amount.

For homeowners insurance, deductibles should reflect potential loss severity, not just premium savings.

Risk Level and Location

Higher-risk environments justify lower deductibles:

Areas prone to storms, wildfires, or theft

High-traffic driving conditions

Businesses with physical operations

Lower-risk situations may allow for higher deductibles safely.

Premium Savings vs Long-Term Cost

Always compare how much you save annually by increasing the deductible. If raising your deductible by $500 only saves $50 per year, it may take many years to break even.

Choose a deductible that offers meaningful savings—not just marginal reductions.

Deductibles by Insurance Type

Auto Insurance

Higher deductibles work well for safe drivers with savings. Lower deductibles may suit commuters or high-risk driving areas.

Homeowners Insurance

Deductibles should be manageable during major losses. Percentage deductibles require extra caution due to their higher out-of-pocket cost.

Renters Insurance

Lower deductibles are often affordable and practical, as premiums are already low.

Health Insurance

High-deductible plans may work if paired with health savings accounts, but only if you can afford medical expenses upfront.

Business Insurance

Deductibles should align with cash flow and risk tolerance. Too high can disrupt operations after a loss.

Common Deductible Mistakes to Avoid

Choosing the highest deductible just to lower premiums

Not considering multiple claims in a short period

Forgetting disaster-specific deductibles

Failing to reassess deductibles as finances change

Assuming higher deductible always means better value

Avoiding these mistakes ensures your deductible supports—not hurts—your financial stability.

How to Reevaluate Your Deductible Over Time

Your deductible choice should change as your situation changes. Review it after:

Income increases

Building an emergency fund

Paying off major debts

Moving to a different risk area

Policy renewals

Annual reviews help keep coverage aligned with reality.

Final Thoughts

The best insurance deductible balances affordability, risk tolerance, and long-term savings. There is no universally “best” deductible—only the one that fits your financial situation and risk exposure.

Choosing wisely protects your budget both today and when you need insurance the most.